If you invest in ETFs in Germany, there’s a good chance your broker will take money from you in January even if you didn’t sell anything. It’s called the Vorabpauschale or ETF Tax and every year it catches investors off guard. Use my tool to quickly calculate your Vorabpauschale

In this guide Ill share:

- What the Vorabpauschale or the ETF Tax in Germany is

- When you pay the ETF Tax (and when you don’t)

- How to estimate your ETF Tax

- The one mistake that can turn this into a paperwork headache

What is the ETF Tax in Germany

Germany treats some ETF gains like they have already been realized, and that’s where this whole “fictitious gain” idea comes from.

The basic intention is: to tax distributing ETFs and accumulating ETFs more similarly.

- With a distributing ETF, you get Dividend payouts So Taxes can be withheld right away.

- With an accumulating ETF, the dividends are reinvested inside the fund. You don’t “receive” cash, so historically you could delay taxes until you sell that’s the tax deferral effect.

To reduce that advantage, Germany introduced the Vorabpauschale: a way to tax a minimum assumed return each year for Funds and ETFs, collected later usually at the start of the year.

The key timing (this is what surprises people)

The timing of this tax is what surprises people: You pay the Vorabpauschale with a one-year delay.

So: the Vorabpauschale or German ETF Tax for the current year is considered “received” on the first working day of the next year, and brokers typically handle the tax around that time. That why you might see a mysterious withdrawal from your account by your broker in January.

But this only happens if you are using a German broker with a connection with the Finanzamt. For international brokers you will have to declare this in your Tax Declaration.

Related Guide: Sending Support to Family from Germany? Here’s How to Claim It on Your German Taxes

ETF Tax (Vorabpauschale) defined

So what exactly is this Vorabpauschale , well it is basically Germany saying:

If your ETF went up, we assume you earned at least some return based on a reference interest rate and we will tax that minimum amount now-ish.

Not your full gain and not a random number. A capped, rule-based “baseline” return.

Calculating the Vorabpauschale (ETF Tax)

Let me share a simple way of calculating the Vorabpauschale. For equity funds and ETFs, you can use the rough method:

- Start with the value of your ETF at the beginning of the year (typically 1 January).

- Multiply by the Basiszins (base interest rate for that year).

- Then multiply by 70% (yes, the law literally uses 70%).

That result is your Basisertrag or (base return). For 2025, the official Basiszins is 2.53%.

So the rough base return rate becomes: 2.53% × 70% = 1.771%

So If you had €10,000 at the start of 2025: €10,000 × 2.53% × 70% = €177.10 base return.

That’s not the tax yet , that’s the amount that might be taxed.

Now The actual taxes: Germany’s withholding tax on capital gains is typically: 25% plus Solidarity surcharge (5.5% on the tax) plus church tax if applicable

And for equity-heavy funds, there’s usually a 30% partial exemption (Teilfreistellung), meaning only 70% of certain fund income is taxable.

So, in many common cases , the effective burden on that base amount ends up somewhere around the “high teens” percent range for equity ETFs which is why people see numbers like 40 to 50 euros per €10k, depending on exact details.

For most people the average would be €36 per €10,000 for equity ETFs as a maximum orientation value, and higher for funds without that equity partial exemption.

Do you ALWAYS pay ETF Tax in Germany?

Now you might ask, do I always pay this vorabpauschale? Well There are three ways or options where the Vorabpauschale is reduced or becomes zero.

1) Distributing ETFs

If your ETF distributed income during the year, those distributions already got taxed. So they reduce the amount of Vorabpauschale left to tax.

2) Your ETF didn’t actually gain enough

The Vorabpauschale is capped by the ETF’s actual price gain in the year.

If your ETF went up only a little, the taxable amount can’t exceed that actual gain.

And if your ETF ended the year down overall? Then there’s no positive gain to “pre-tax” so the Vorabpauschale can be zero.

3) Basiszins is zero/negative

If the Basiszins is effectively not positive, the whole mechanism can collapse to zero. This is exactly why most of you never really heard about this tax. As in recent history the effective interest rate only became positive since 2022 so many investors saw no Vorabpauschale.

Related Guide: Learn 80% about Taxes in Germany in under 13 Minutes

What you should do right now

A few things you must do right after you finish watching this video if you do not want to face addtional paperwork is

Step 1: Make sure your Freistellungsauftrag is set

In Germany you get a saver’s allowance (Sparer-Pauschbetrag):

- €1,000 per person

- €2,000 for married couples filing jointly

If your Freistellungsauftrag is active and not already used up, your broker can use it to cover taxes including the Vorabpauschale.

This tax tax event happens in early January for the prior year’s Vorabpauschale, so the relevant allowance is basically your new year’s allowance (fresh, unused… unless you instantly used it elsewhere). This is why, for many people, January is actually the “least painful” month for this tax.

Step 2: Keep enough cash in the settlement account

If your allowance doesn’t cover it (or you didn’t set it), your broker will try to withhold the tax from your cash balance.

And if your cash balance is zero because you’re fully invested?

Then you can get into the annoying zone.

Some banks can pull from other linked accounts (like a Current account at the same bank). Others cannot. And brokers differ a lot in how they handle it.

So If the broker can’t collect, they may notify you and if it remains unpaid, you may end up having to handle the capital income via your tax return using the form KAP. This is also what you would have to do if your investing app is not German and not connected with the Finanzamt.

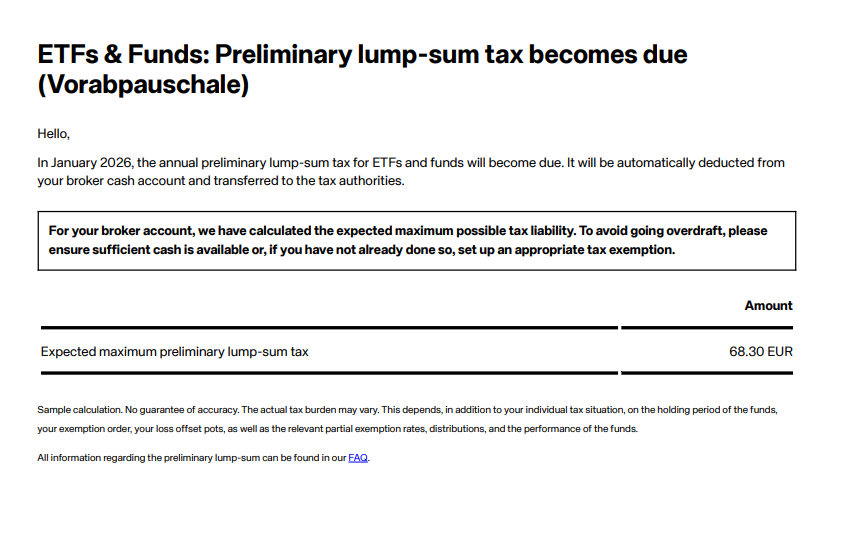

For people who are using Scalable Capital, you should receive a letter from Scalable Capital regarding the Vorabpauschale by the beginning of December.

This is what I got from them. This clearly states how much Preloiminary lump-sum tax is due from my Scalable Capital Portfolio.

The also recommend adding additional funds into my account is this tax is higher than my tax exemption order. In my case the amount is quite small and my tax free allowance can easily cover this tax.

You can also find this letter by going to your profile then Mailbox and then the Preliminary lump-sum message.

In any case I would recommend adding about 50€ per 10 thousand euros invested in ETFs to your Investment account as cash just to be safe.

ETF Tax on Savings plans

What about savings plans? How does one calculate the Vorabpauscale for that?

This is where things get interesting, because each monthly buy was held for a different fraction of the year. Here the “base return” part is effectively weighted by months held, the earlier in the year you bought, the more it counts.

So your June purchase might count for roughly half of the year, while your December buy counts for 1/12.

This is why if you invest using a Dollar Cost Ageraging method or SIP you either accept a rough estimate, rely on broker reporting or tools that do the heavy lifting.

Remember that paying Vorabpauschale doesn’t mean you’re getting double-taxed forever, amounts paid can matter later when you actually sell, because the system tracks taxation over time.

This article contains Affiliate links, I may earn a commission if you use the link and make an account at no additional cost to you

Disclaimer: None of the content in this article is meant to be considered as investment advice, as I am not a financial expert and am only sharing my experience with stock investing. The information is based on my own research and is only accurate at the time of posting this article but may not be accurate at the time you are reading it.