The new SCHUFA score has recently been launched, and for the first time, it gives people much more transparency about how their credit score in Germany is calculated.

Previously, the SCHUFA score felt like a black box. Many people did not really know what affected their creditworthiness or why their score changed. Now, the new SCHUFA score is clearer because SCHUFA has published the 12 criteria that count towards your credit score in Germany.

On paper, this is a good thing. More transparency is always better than guessing.

But when you look at the details, there are some points that can negatively affect expats, especially people who are new to Germany.

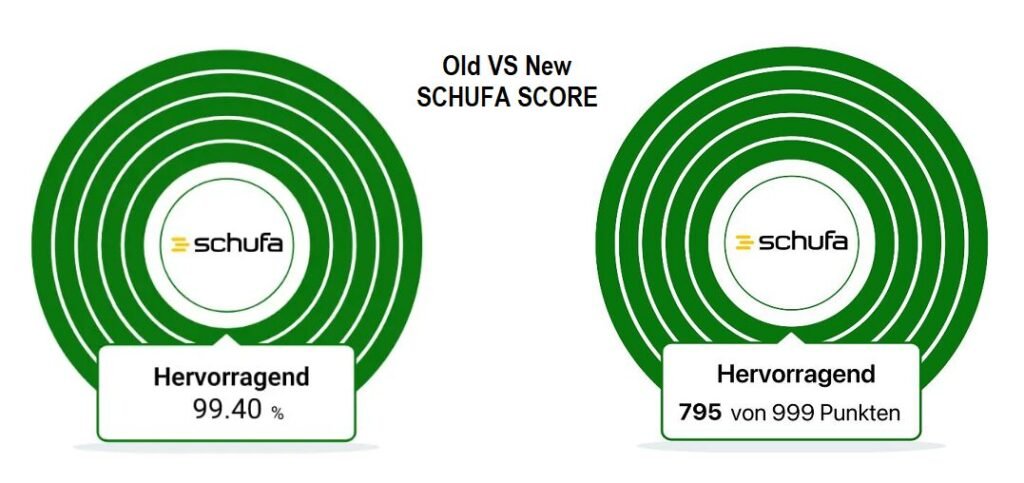

Before this new SCHUFA score was launched, my old SCHUFA score usually fluctuated between around 99.88% and 98.9%. But with the new scoring system, my score is currently around 750 points.

So, let me explain how the new SCHUFA score works, what the 12 criteria are, and why I think this system may not be great for expats in Germany.

How to Check Your SCHUFA Score for Free

To get your SCHUFA score, you need to register with SCHUFA’s service. The registration is free and you can get your FREE SCHUFA SCORE HERE.

You only need to sign up with your phone number and email address. Once you have registered, you can access your SCHUFA score for free.

The new score is shown on a scale from 100 to 999 points. The higher your score, the better your creditworthiness is considered to be.

SCHUFA divides the new score into different score classes:

| SCHUFA Score | Score Class |

|---|---|

| 776 to 999 points | Excellent |

| 709 to 775 points | Good |

| 642 to 708 points | Acceptable |

| 100 to 641 points | Sufficient |

| Open payment disruption | Insufficient / no normal score class |

Now let’s go through the 12 criteria that can affect your credit score in Germany.

1. Payment Disruptions

The first and most important factor is payment disruptions. If you use a service in Germany and fail to pay your bills, this can lead to a payment disruption. The more serious or recent the payment disruption is, the worse it is for your SCHUFA score.

For example, if you joined a gym and forgot to pay one of the invoices, this could potentially become a payment disruption if the case is reported to SCHUFA.

The scoring works like this:

| Situation | Points |

| Open payment disruption | No normal score / insufficient |

| Previous disruption resolved within this year | 100 |

| Previous disruption resolved at least one year ago | 135 |

| No payment disruptions | 264 |

This means that payment disruptions can cost you up to 264 points.

That is huge. It can be the difference between getting decent interest rates and contract conditions, or not being accepted for certain financial services at all.

This is why it is important to check your SCHUFA score regularly. For expats in Germany, this is especially important. If you are new here or have moved recently, make sure your old addresses are updated with all contract providers.

Sometimes bills or letters are sent to your previous address. If you no longer live there, you may miss the payment reminder and unintentionally damage your SCHUFA score.

2. Recent Bank Account or Credit Card Applications

The second factor is recent applications or openings for current accounts and credit cards. The fewer applications or openings you had in the last 12 months, the better it is for your score.

There is also a difference between an inquiry and an opening.

For example, if you apply for a bank account, this can already count as an inquiry. It does not necessarily matter whether the bank account was actually opened or not.

The scoring works like this:

| Applications or openings in the last 12 months | Points |

| 0 | 117 |

| 1 | 82 |

| 2 | 44 |

| 3 or more | 0 |

This can be a negative point for people who constantly switch bank accounts to get better interest rates, bonuses, or short-term offers.

Instead of account hopping, it may be better to find a good bank account with decent conditions and keep it for a longer period.

This is especially important for expats, because many people first open one account when they arrive in Germany and then later switch again once they understand the banking system better. That is understandable, but too many applications in a short period can reduce your score.

3. Inquiries Outside the Banking Sector

The third category is inquiries outside the banking sector. This can include things like:

- Online retailers

- Telecom contracts

- Installment payment checks

- Buy-now-pay-later options

- Similar credit checks outside traditional banking

Many people do not think that these types of payment methods can affect their SCHUFA score. But with the new SCHUFA score, these inquiries clearly matter.

The scoring works like this:

| Inquiries outside the banking sector in the last 12 months | Points |

| 0 or 1 | 99 |

| 2 | 71 |

| 3 | 40 |

| 4 or more | 0 |

This means that even if you are not applying for a loan or a credit card, certain types of payment options can still affect your score. So, if you want to protect your SCHUFA score, try to avoid unnecessary installment payment options or credit checks, especially for small purchases.

For example, buying a phone, furniture, or electronics in installments may look convenient, but it can also create additional credit checks.

4. Age of Your Current Address

The next factor is the age of your current address. This is one of the strangest criteria, especially from an expat perspective. The longer you live at the same address, the more points you can get.

The scoring works like this:

| Time at current address | Points |

| Less than 7 months | 0 |

| More than 7 months | 6 |

| Around 15 years | 75 |

| Around 20 years | 94 |

This is great for people who have a very stable life and have lived at the same address for many years. But for expats, this is one of the categories where many people will automatically lose points.

Expats often move when they first arrive in Germany. You may start in temporary accommodation, then move to your first proper apartment, then maybe move again because of work, family, or a better housing situation. That is completely normal. But under this scoring system, frequent moves or a short address history can reduce your score.

So, where possible, try to keep your address consistent and avoid unnecessary moves. This is especially important if buying real estate is part of your near-term plan. If you want to buy property in the next two to three years, your SCHUFA score can matter for financing conditions.

5. Age of Your Oldest Bank Contract

The fifth factor is the age of your oldest bank contract. This is another area where you can lose points if you frequently change bank accounts. A longer and more stable banking history can help your SCHUFA score.

The scoring works like this:

| Age of oldest bank contract | Points |

| No bank contract | 18 |

| Less than 3 months | 0 |

| Around 3 months | 3 |

| Around 1 year | 12 |

| Around 4 years | 23 |

| Around 10 years | 49 |

| Around 20 years | 69 |

Interestingly, according to this scoring system, having no bank contract can be better than having a very new bank contract.

This is not great for people who are new to Germany, because when you first arrive, your German bank account will obviously be new.

There are two practical ways to look at this. First, when you arrive in Germany, try to choose a bank account that you are comfortable keeping for a long time.

Second, if you currently have a temporary or unsuitable account, it may be better to change it early instead of switching repeatedly later.

6. Age of Your Oldest Credit Card

The sixth factor is the age of your oldest credit card. If used properly, a credit card can be useful in Germany. You may not get the same level of credit card benefits as in the US or some other countries, but a good credit card can still make sense.

For example, some credit cards may offer:

- Travel insurance

- Baggage insurance

- Rental car benefits

- Better payment flexibility while travelling

The scoring works like this:

| Age of oldest credit card | Points |

| No credit card | 24 |

| Older than 6 months | 14 |

| Around 15 years | 81 |

This is an interesting one.

If you do not have a credit card, you still get 24 points. But if you have a relatively new credit card, you may get fewer points than someone with no credit card at all. Over time, however, an old credit card can become positive for your score.

Still, I would not recommend opening a credit card only for the SCHUFA score. You should open one only if it has actual utility for you.

For example, if you travel often, need a card for rental cars, or want certain insurance benefits, then having a credit card can make sense.

Personally, I prefer the TF Bank credit card.

Related Guide: TF Bank Credit Card Review – Its Advantages and Disadvantages!

7. Identity Verification

The seventh factor is identity verification.

When you get your SCHUFA score, you can add your identity details to SCHUFA. But if you fully verify your identity, you can receive additional points.

The scoring works like this:

| Identity status | Points |

| Identity not verified | 0 |

| Identity verified | 38 |

This is one of the easier points to improve because it does not require changing your financial behaviour. You simply need to complete the identity verification process.

For expats, this is one of the first things I would check because it is relatively simple compared to improving address history or contract age.

8. Age of Your Youngest Framework Credit

The eighth factor is the age of your youngest framework credit.

A framework credit is a type of credit line where you can use an approved credit amount flexibly. In German, this is usually referred to as a Rahmenkredit. The good thing here is that if you do not have any framework credit, you do not lose points. In fact, you can receive the full 36 points.

The scoring works like this:

| Youngest framework credit | Points |

| No framework credit | 36 |

| Less than 1 year old | 0 |

| At least 1 year old | 16 |

| At least 2 years old | 36 |

So, if you do not understand framework credit or do not need it, it may be better not to open one unnecessarily. For most expats, this is not something I would actively chase.

9. Installment Loans in the Last 12 Months

The ninth factor is installment loans in the last 12 months. The fewer installment loans you have, the better it is for your score.

The scoring works like this:

| Installment loans in the last 12 months | Points |

| 0 | 66 |

| 1 | 48 |

| 2 | 32 |

| 3 or more | 0 |

As an expat, I would generally try to avoid installment loans as much as possible, especially for consumer purchases. This includes things like financing furniture, electronics, phones, or other lifestyle purchases.

Installment loans can affect your SCHUFA score and may also reduce your financial flexibility.

10. Longest Remaining Term of Installment Loans

The tenth factor is connected to installment loans again.

This criterion looks at the longest remaining term of any installment loan you currently have.

The scoring works like this:

| Longest remaining installment loan term | Points |

| No installment loan | 61 |

| Up to 3 years remaining | 61 |

| From 3 years remaining | 48 |

| From 4 years remaining | 28 |

| From 5 years remaining | 10 |

| From 6 years or more remaining | 0 |

So, long-running installment loans can negatively affect your score.

This is another reason to be careful with financing consumer purchases over many years.

A small monthly payment may look harmless, but a long loan term can still affect your financial profile.

11. Credit Status of Installment Loans

The eleventh factor is whether you have successfully completed an installment loan. This is a slightly strange part of the scoring system. If you have completed an installment loan successfully, you get more points than someone who has never had an installment loan.

The scoring works like this:

| Credit status | Points |

| Successfully completed installment loan | 19 |

| No installment loan | 9 |

| Open or negatively completed installment loan | 0 |

So, in this specific category, having successfully completed a loan gives you more points than never having had one. But this does not mean that you should take out a loan just to improve your SCHUFA score.

When you compare this category with the previous installment loan categories, unnecessary loans can still hurt you more than they help you. In most cases, avoiding unnecessary debt is still the better financial decision.

12. Real Estate Loan or Guarantee

The final factor is real estate loans or guarantees.

If you have a real estate loan, or if you are a guarantor for someone else’s real estate loan, you can receive additional points.

The scoring works like this:

| Situation | Points |

| Real estate loan or guarantee | 55 |

| No real estate loan or guarantee | 0 |

This is another factor where expats may be at a disadvantage.

Many expats do not own property in Germany, especially in the first few years after arriving. So, they automatically miss out on these points.

This is why the new SCHUFA score may feel unfair for many expats.

You may be financially responsible, have a good income, save money, and pay your bills on time, but still miss out on points simply because you do not have a long financial history in Germany.

Why the New SCHUFA Score May Be Bad for Expats

The new SCHUFA score gives us more transparency, which is a good thing. But when you look at the 12 criteria, it becomes clear that the system rewards long-term stability in Germany.

You may benefit if you have:

- Lived at the same address for many years

- Had the same bank account for a long time

- Had the same credit card for a long time

- No recent applications or inquiries

- No payment disruptions

- A long financial history in Germany

- A real estate loan or completed credit history

The problem is that many expats simply cannot have these things when they first arrive in Germany.

New expats often have:

- A short address history

- A new bank account

- No old German credit card

- No long-term German credit history

- More recent applications for basic financial services

- No real estate loan

- No completed German loan history

So even if you are financially responsible, earn a good salary, pay your bills on time, and manage your money well, you may still not get an excellent SCHUFA score simply because you are new to Germany.

That is why I think the new SCHUFA score is clearer, but not necessarily good for expats.

What Expats Can Do to Improve Their SCHUFA Score

You cannot change everything immediately, but you can take a few practical steps.

Try to:

- Pay all bills on time

- Keep your address updated with all contract providers

- Avoid unnecessary bank account and credit card applications

- Avoid unnecessary credit checks outside the banking sector

- Avoid installment payments for small purchases

- Keep a stable bank account for the long term

- Keep a useful credit card open if it makes sense for you

- Avoid unnecessary loans

- Verify your identity with SCHUFA

- Check your SCHUFA score regularly

The goal is not to chase every single point.

The goal is to avoid easy mistakes that can damage your credit profile in Germany.

My SCHUFA Tool for Expats in Germany

I have turned everything in this article into a tool named “Schufa Check: SCHUFA Score Companion“

I have also created a SCHUFA quiz that helps you understand which points you should focus on based on your own situation.

There is also an action checklist that can help you improve your SCHUFA score step by step.

Final Thoughts

Overall, I think the new SCHUFA score is useful because it provides more clarity than before.

But for expats in Germany, I think the system is still a bit negative.

It rewards long-term stability, old contracts, old addresses, and long credit history. These are things that many expats simply do not have when they first move to Germany.

So, if you are new in Germany, do not panic if your score is not perfect.

Focus on the things you can control: pay your bills on time, avoid unnecessary credit checks, keep your financial life simple, and build your history slowly.

Over time, your SCHUFA score can improve.

This article contains Affiliate links, I may earn a commission if you use the link and make an account at no additional cost to you

Disclaimer: None of the content in this article is meant to be considered as investment advice, as I am not a financial expert and am only sharing my experience with stock investing. The information is based on my own research and is only accurate at the time of posting this article but may not be accurate at the time you are reading it.