Have you ever wondered how much money you need to make to buy a house in Germany? well wonder no longer because today we’ll cover exactly how much house you can afford in Germany!

This is how much house you can afford in Germany

Loan as a Percentage of your salary in Germany

As a rule of thumb, your maximum monthly payment on a loan should not exceed 35% of your monthly net household income.

However Interest rates in Germany are the highest they have been in the last decade. But the low interest rate in the past caused the housing market to soar thats why Houses in Germany are more expensive than they have ever been.

On top of that the lack of new constructions is making the prices for real estate in Germany even greater. This is why more than half of the population in Germany rents a house. But you are thinking of buying a house in germany and want to know if it is possible for you to buy a house in Germany or not?

Rent vs Buy a house in Germany?

When it comes to housing expenses it’s important to understand that there is a huge difference between buying and renting. As you’re about to see the costs are going to be substantially different depending on which route you decide to go.

For example your rent is the most you'll ever pay each month and your mortgage is the least you'll ever pay.

As a renter you pay your “Kaltmiete” or the cold rent at a fixed cost and the “Nebenkosten” or the additional costs are somewhat variable. But you generally pay them based on your usage. There aren’t going to be any surprise bills or urgent repairs that can drain your bank account.

Where as when you buy a house, well you have your mortgage , if anything gets broken you have to get that fixed, then there are insurance costs, gardening fees and so much more which I will be discussing in detail.

Most Esssential Part of Buying Real Estate in Germany

Buying or building a house in Germany is a decision that many of us would probably only make once in our lives. and that presents us with major financial challenges. That’s why the first step on the way to your dream property is the question of the financial leeway . In order to determine this, you have to answer for yourself three questions:

- What monthly burden can I cope with?

- How high are my financing needs?

- What loan rate results from my financial flexibility?

Exactly How much House can you Afford in Germany?

As I mentioned in the beginning, most people use a rule of thumb, having a maximum loan of less than 35% of your monthly net income.

To calculate this just take your monthly income multiply that by 0.35 and that’s how much your payment should be .

Lets assume your monthly salary is €3500 so your maximum mortgage/loan amount should be less than 3500x0.35 = €1225 per month

This amount is enough to buy a home in the €200.000 range with 20% down payment at a 3.5% interest rate. Ofcourse if you’re disappointed that a €65.000 salary in Germany is only enough to afford a €200.000 home you’re not alone.

If you want something to blame it’s

- The extremely low interest rates in the last ten years

- The German beurocracy and

- The horrendously low amount of real estate being built in Germany.

German Housing affordability in 2026 vs 2022

Just consider that when mortgage rates were at sub one percent (2022). The typical €65.000 income was enough to buy a home in the €250.000 range. But now with costs having increased that final number is significantly lower.

That’s why under the 35 percent rule you would need to be making €120.000 a year to buy a €500.000 house in Stuttgart or €250.000 per year to purchase a €1.000.000 house in Munich. With monthly loan installements of 2000 and 4000euros respectivly .

With the 35% rule the monthly loan installment should always be lower than your financial resilience!

Calculate how much loan you can afford in Germany

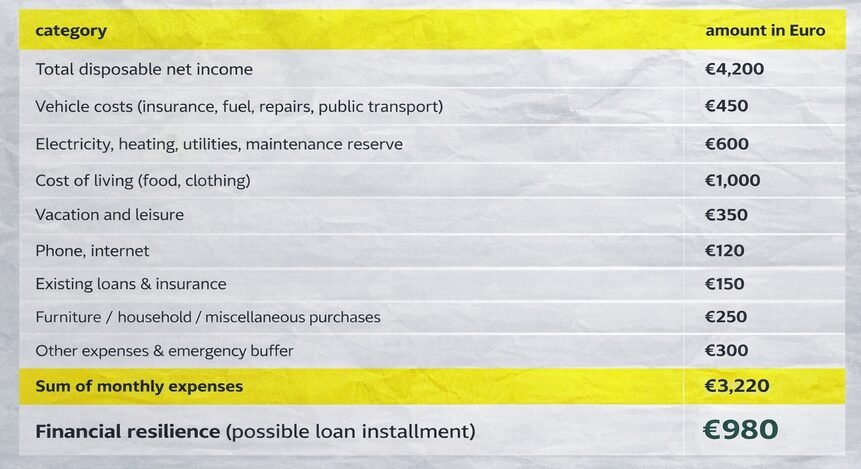

A monthly bill of expenses or household account is a good starting point for determining the possible monthly loan installment . It is best to use tables to record all monthly household costs, special expenses and living expenses.The difference now shows you your individual financial resilience .

Potential loan borrowers in Germany who fully and continuously record their expenses do not have to expect any unpleasant surprises with their finances. A sample calculation for a family of three might look like this:

What expenses can you expect when Buying a House in Germany?

House owners do save on the rent, but still have to bear heating, electricity, water, sewage and waste costs. That is why some people use the €2 rule which says you’ll spend €2 for every Square meter of livable space every single year for homes or apartments in Germany.

You should also put money aside for maintenance, repairs and renovations on the house that will sooner or later require a lot of money. If the planned financial reserve is not used up every month, this amount can be used as a reserve for future expenses.

Remember: This calculation does not include any other investment options like stocks and ETFs.

Reality Check for Home Buyers in Germany

The household account is the basis to determine how much house your can afford in Germany. Because without looking at the household finances, you will not have an overview of your liquidity. In particular, you need to know what expenses you will incur. However, a household bill alone is not enough. You also have to consider the key factors involved in financing a house as well.

It will definitely benefit you to have an honest and realistic check. The more precisely you estimate your income and expenses, the less likely it is that the financing calculation will fail. A monthly budet , for example, is a good helper when recording income and expenses.

Why you need an Emergency Fund before buying a House in Germany

To be on the safe side, please also include an Emergency Fund so that unplanned costs do not lead to future problems with your loan repayment. Have you considered what you would do if you or your partner lost their job? How many months would you be able to survive without a job?

I want you to include this variable in your calculations because just a couple of days ago someone I know got terminated from their job and they are now in huge financial problems becasue they are not able to pay the installements on their loans.

So you have deducted the regular and sporadic expenses from the long-term secured income and you have figured out your financial resiliance? Next we will discuss The role of equity in budget determination.

How much down payment is needed to buy an apartment in Germany?

Unless you have been saving for many year or hit the jackpot it is unlikely that you would be buying a house in Germany with your own resources. Thats why you are going to need real estate financing.

When you take out a loan you can pay monthly installements and those include an interest and repayment component. It is important to know that the more equity you bring in, the lower the monthly financing burden. As equity lowers the interest cost of your home loan.

What exactly can be included in Equity?

As someone who is interested in Buying a house in Germany, Real estate buyers can include:

- Cash

- Funds in Bank accounts

- Securities such as Stocks or ETFs

- Life insurance payouts

And many others but all of these depend on whether you want to get a loan on a property you want to build or buy.

Good down payment amount to buy German Real Estate

Banks assume that around 20 to 30 percent equity is good for Real Estate financing. This is essential to how much house you can afford in Germany. Because the less real estate loan you need, the lower your repayment amount to the bank.

When buying a house without equity, borrowers have to have a credit rating that is beyond any doubt and must be able to service high monthly loan installments. This type of real estate financing is therefore only an option in exceptional cases.

Getting a Home Loan in Germany on Blue Card

One thing to note here is that In one of my articles that a while ago, I mentioned that it was not possible to get a loan if you had a blue card. This was based on my personal experience but since then I have seen many cases of people getting a home loan in germany even being on a blue card.

How to reduce interest rate on German Home Loan

The percentage of funds you bring as a down payment doesn’t just reduce your credit ratio. Borrowers with high equity also receive better conditions than other borrowers.

A lot of savings therefore means lower debit interest for your loan. The high proportion of equity would also give you a good credit rating. Anyone who has already saved up their own funds is considered trustworthy and disciplined by banks. Make sure that you keep you Emergency fund separate from the equity.

So you have calculated your Financial Resiliance, you know how much equity you can bring in. What else is needed to find how much house you can afford in Germany?

Cost most new home buyers in Germany forget to calculate

One of the biggest expenses you need to consider is the “Nebenkosten” or the Additional costs of buying a house in Germany.

Banks usually do not finance any additional purchase costs. You as the borrower must cover at least these costs from their own funds. Depending on the federal state in which the property is located, this is between around 10 and 15 percent of the purchase price.

These costs should not be underestimated, as they play a huge role in figuring out how much house you can afford in Germany. And include:

- 3.5 to 6.5% Property transfer tax

- 1% Notar costs

- 1% for Entry into the land register

- 3 to 6% Broker costs of between

When are additional costs due?

You should know that these additional costs for buying a property in Germany are due for payment at the notary immediately after the purchase contract has been concluded.

The involvement of a notary is required by law to protect homebuyers from hasty and ill-considered purchase decisions. The notary fees cannot be negotiated arbitrarily, but depend on the property purchase price and have been uniformly regulated by the law.

That is why When planning your budget, be sure to also take into account the additional costs. If these costs are not included, the budget will lack money for the loan repayment or maintenance of the property in the short or long term.

Less common costs of buying a house in Germany

There are other costs that you should consider too like:

- Expenses for moving and new furniture

- If necessary, modernization or repair costs, trust me you will need to do some repairs when you buy you a house in Germany. It wont be necessary but you will do them never the less.

Dont forget, the ongoing additional costs weighing on your monthly budget. They include the annual property tax as well as insurance premiums for home insurance and natural hazard insurance.

Before you buy a house in Germany

Just keep in mind that these are General guidelines and there’s nothing that says you can’t split this cost with the partner, live with roommates or spend a different amount. Thats why If you want to invest in German Real Estate Don’t buy a home in Germany without reading this article.

This article may contain Affiliate links, I may earn a commission if you use the link and make an account at no additional cost to you

Disclaimer: None of the content in this article is meant to be considered as investment advice, as I am not a financial expert and am only sharing my experience with stock investing. The information is based on my own research and is only accurate at the time of posting this article but may not be accurate at the time you are reading it.